Improving your Digital Identity with Okra

Building a KYC/KYB system in a digital financial business is difficult, considering the increase in fraud and the constant change of regulations.

Credibility, consistency, and security are the hallmarks for guaranteeing a sustainable digital identity system. At Okra, we’re committed to ensuring that digital identity activities are carried out hassle-free via secured channels.

For verification purposes, many digital businesses request access to your identity, financial, or business information before providing you with their services. In other words, you have some apps that require you enter your BVN to verify your identity or RC/TIN to verify your identity/business. While this is common to most products, many individuals are concerned about data privacy and might be skeptical about sharing their BVN across too many apps. I mean, what if something goes wrong? Asides from that, there’s a recent BVN ban by the regulation body guiding the affairs of finance in Nigeria on non-financial banking products to provide BVN services, which means BVN services will no longer be a means of identity verification among fintech products.

For example, from your perspective, you’re building a digital banking service. With the current BVN ban, you’re unsure how you can validate user identities after signing up on your platform. Confusion sets in. You probably have to wait for a newer means of validation to be announced, which could open the room to fraud and multiple unverified identities.

The big questions are, is it possible to still validate a user’s identity? What steps are needed to do so? These questions are perhaps in the corner of your heart, waiting for answers.

How Okra solves the Identity problem for your business

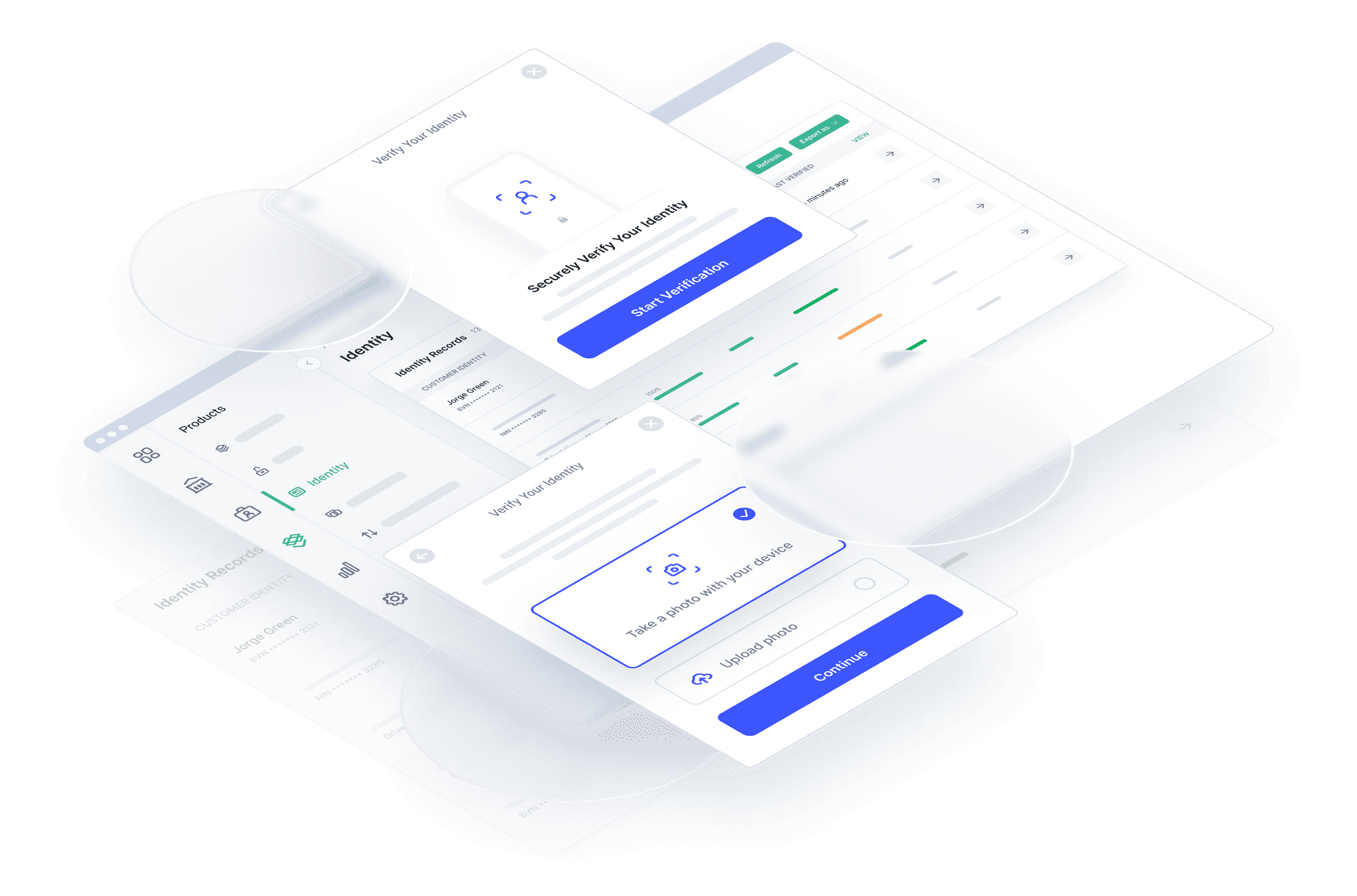

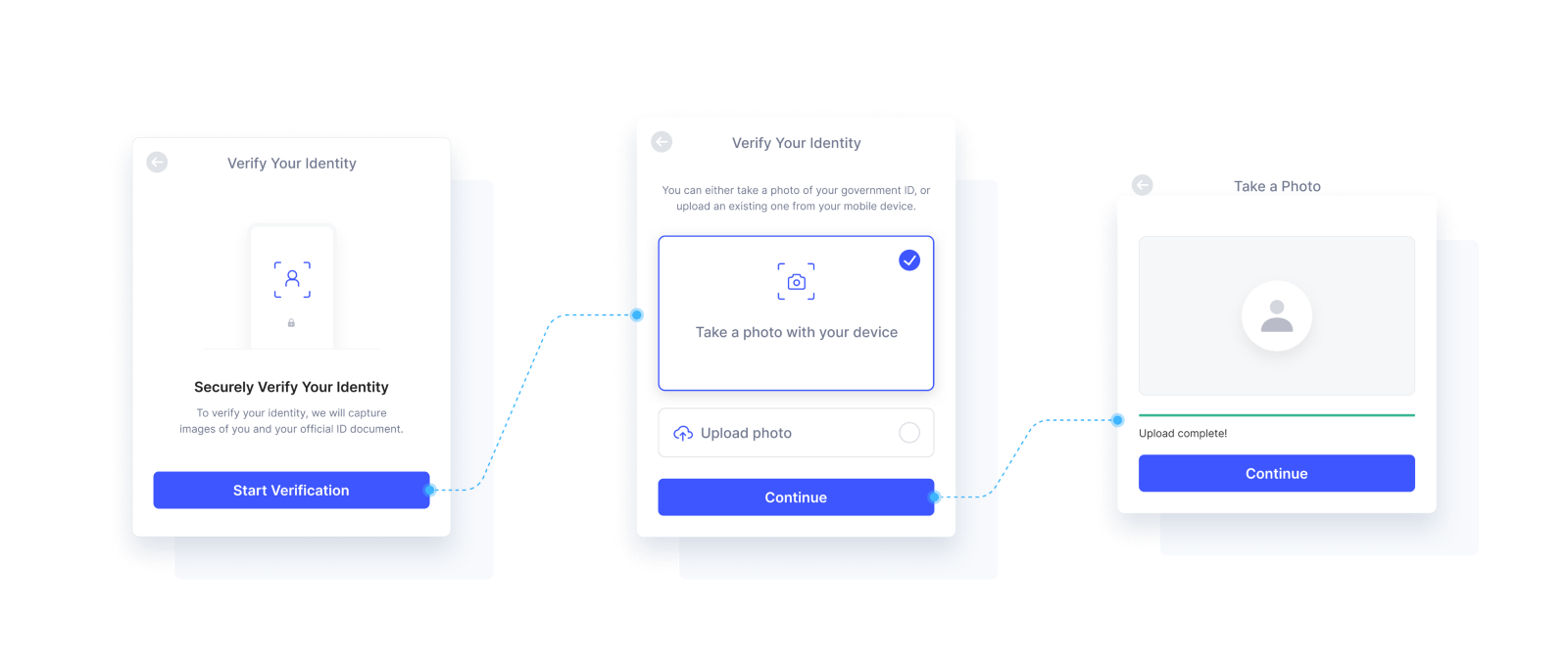

At Okra, we make the Identity Verification process flawless. It happens in a matter of seconds without demanding too much from a customer. We combine identity validation with ownership to reduce risk and fraud.

Without the ability to digitally validate an end user’s identity in real-time, consumers may be forced to upload and send emails containing sensitive information manually or — even worse, submit a paper application. These methods are less secure and less efficient than Okra’s automated and real-time alternative.

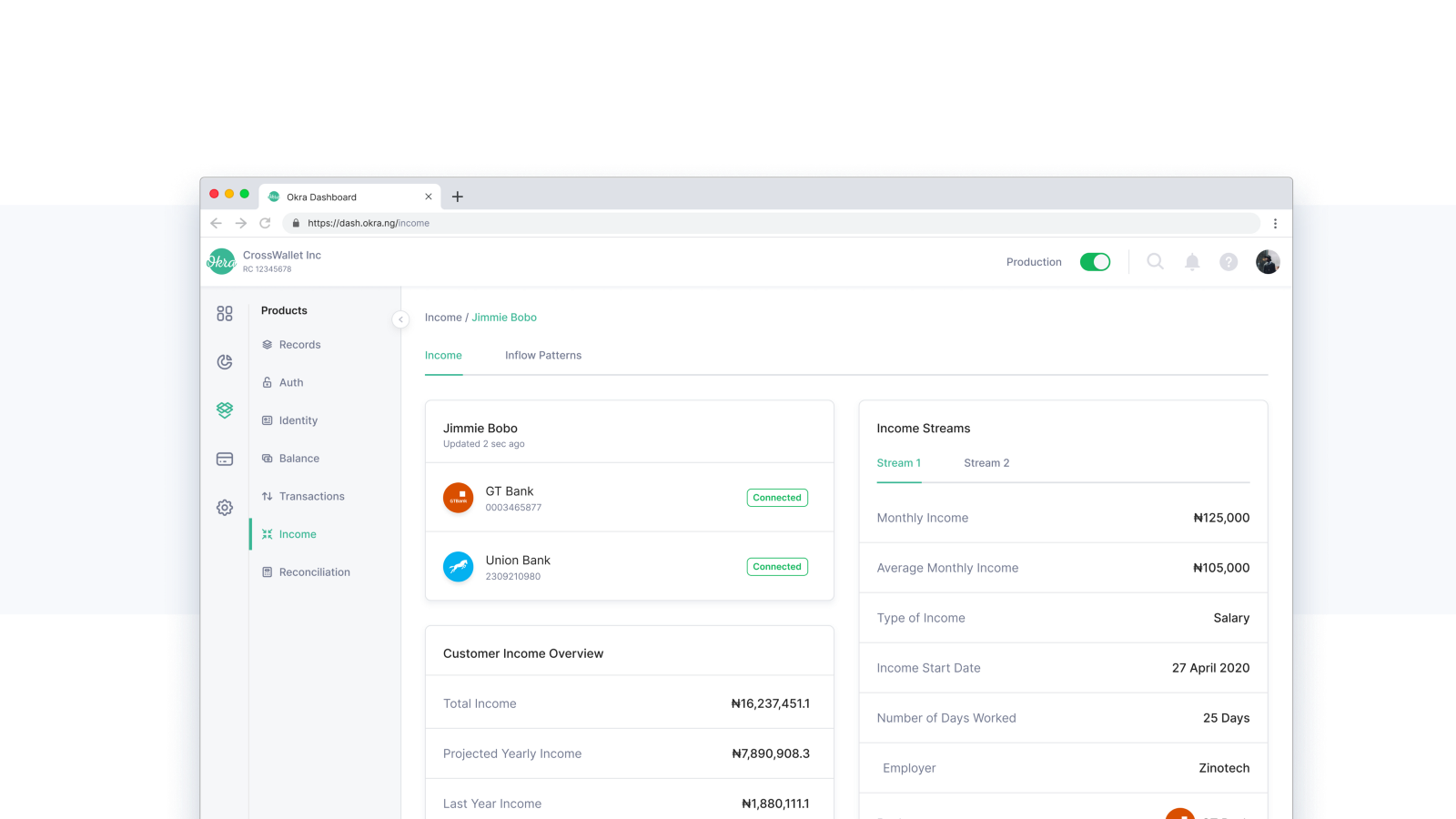

During onboarding with the Okra widget, users will need to link their bank account to your product by entering their internet, mobile banking details, or via our USSD channels. When account linking is completed, it permits Okra to retrieve the user’s bank data securely.

It returns a response that contains a complete user profile, and this response includes the following:

- Validated BVN, NIN, or RC Number

- Validated Company Registration and Tax Details(corporate entities only)

- Biometric Photo ID

- DTI (Debt-to-Income score)

- Mother’s Maiden Name*

- Full Name or Company Name

- Alias(es)

- Gender

- Date of Birth

- Email Address(es)

- Addresses

- Phone number(s)

Throughout the process, users are in control of their personal information, they only give the needed permissions to the relevant financial institutions before their details can be retrieved. This is a lot easier than the previous means of verifying user identity with BVN.

Alternatively, Okra has other means of verification such as NUBAN and RC/TIN retrievals that help improves your business operations, digitise your processes, and make your business less prone to fraud.

Okra Identity and Selfie Verification

Onboarding (KYC/KYB) is one of the most essential processes for digital services, yet it’s currently the most painful part of the process. Okra’s selfie verification enhances identity validation by ensuring your customer is who they say they are — by allowing them to take a selfie photo you can pass on to Okra API, which will validate it against their biometric photo ID. This makes the KYC process more frictionless and dynamic, which significantly reduces the possibility of fraud by confirming the person using your product is the account owner at the validated bank.

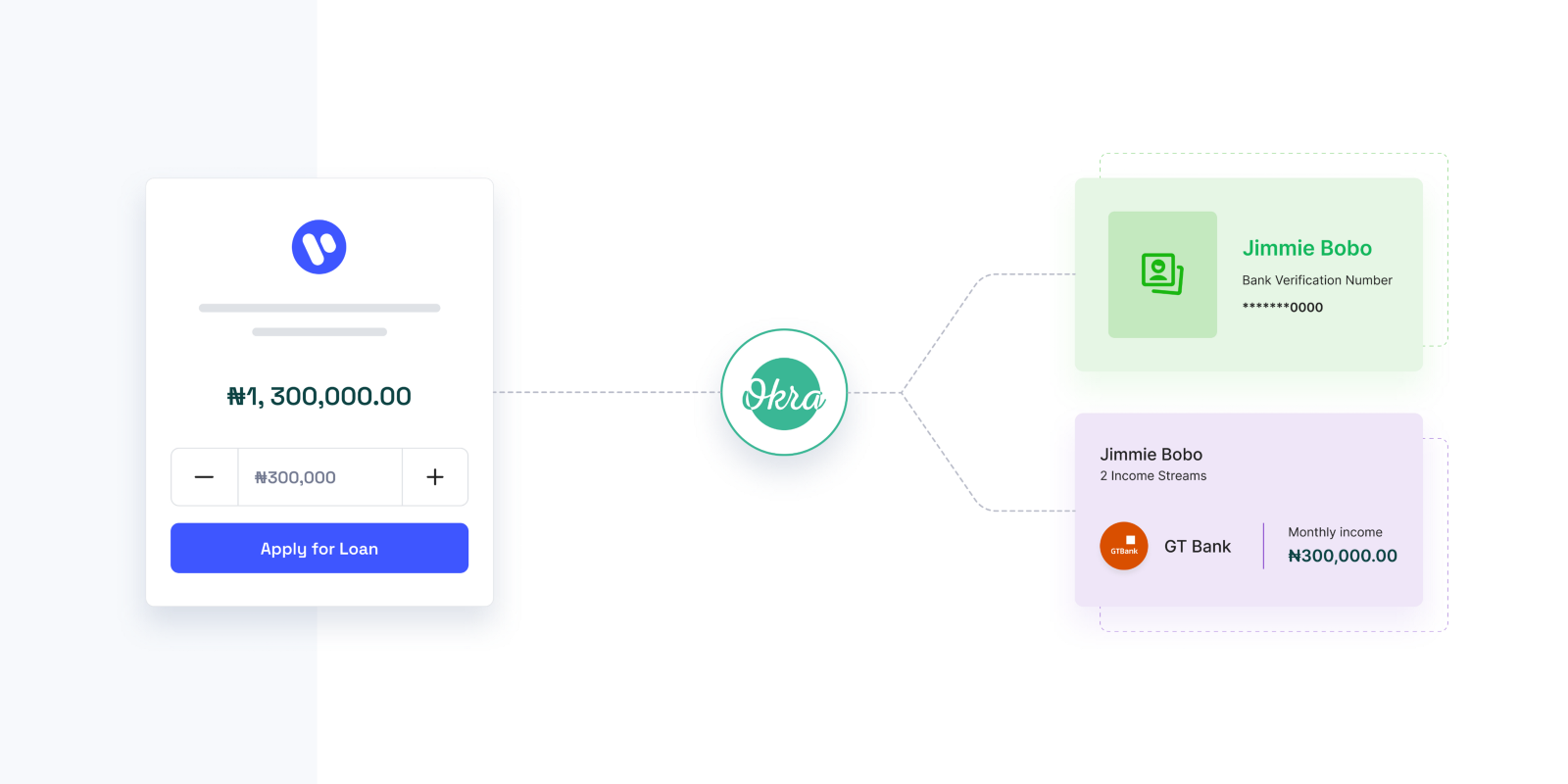

Okra Identity with Income

For businesses that offer loan services to users, it might come in handy to verify the income, the salary of a user before issuing the loan. With the Okra Income-Identity process, the digital business can validate all the structured and unstructured income sources of a customer.

Understanding a user’s current and past earning history over a 3 to 24-month period can unlock critical eligibility information, such as employment verification, spending patterns. These can all be used for vital eligibility use cases, including disbursement amounts, product recommendations, payment tenures, and more. Income provides a wealth of opportunities for KYC validation.

Companies Building With Okra Identity

These are some of the companies building with Okra Identity— you’re not alone. 😇

Conclusion

Now that you know how it works, a good place to start is to check out our docs and if you are passionate about open finance, you definitely should visit our website at https://okra.ng, to see other services that might be appealing to you.

Contact sales or send an email to sales@okra.ng to get started!